June 6, 2026

The money meta: every online gold rush since 2010, and where AI agents really are on the curve

Casino, affiliate, e-commerce, crypto, courses, AI. Every few years the online money meta rotates. Here's the pattern, the law underneath it, and why AI automation is the 2018-e-commerce moment, not the top.

TL;DR

- The online money meta rotates every 2–4 years: casino, affiliate, e-commerce, crypto, courses, AI. Same operators, new arbitrage.

- The law underneath it: an arbitrage opens, early movers extract, it gets commoditized and regulated, the caravan moves.

- The 2026 shift is structural — the AI agent is becoming the customer, so value migrates to distribution, trust, regulatory access, and data.

- AI automation is not saturated. It’s the 2018-e-commerce moment: loud on the operator side, barely penetrated on the demand side.

- The bar has moved from “be early” to “deliver measurable ROI in a vertical.” The runway is five years, but it rewards depth, not copy-paste agencies.

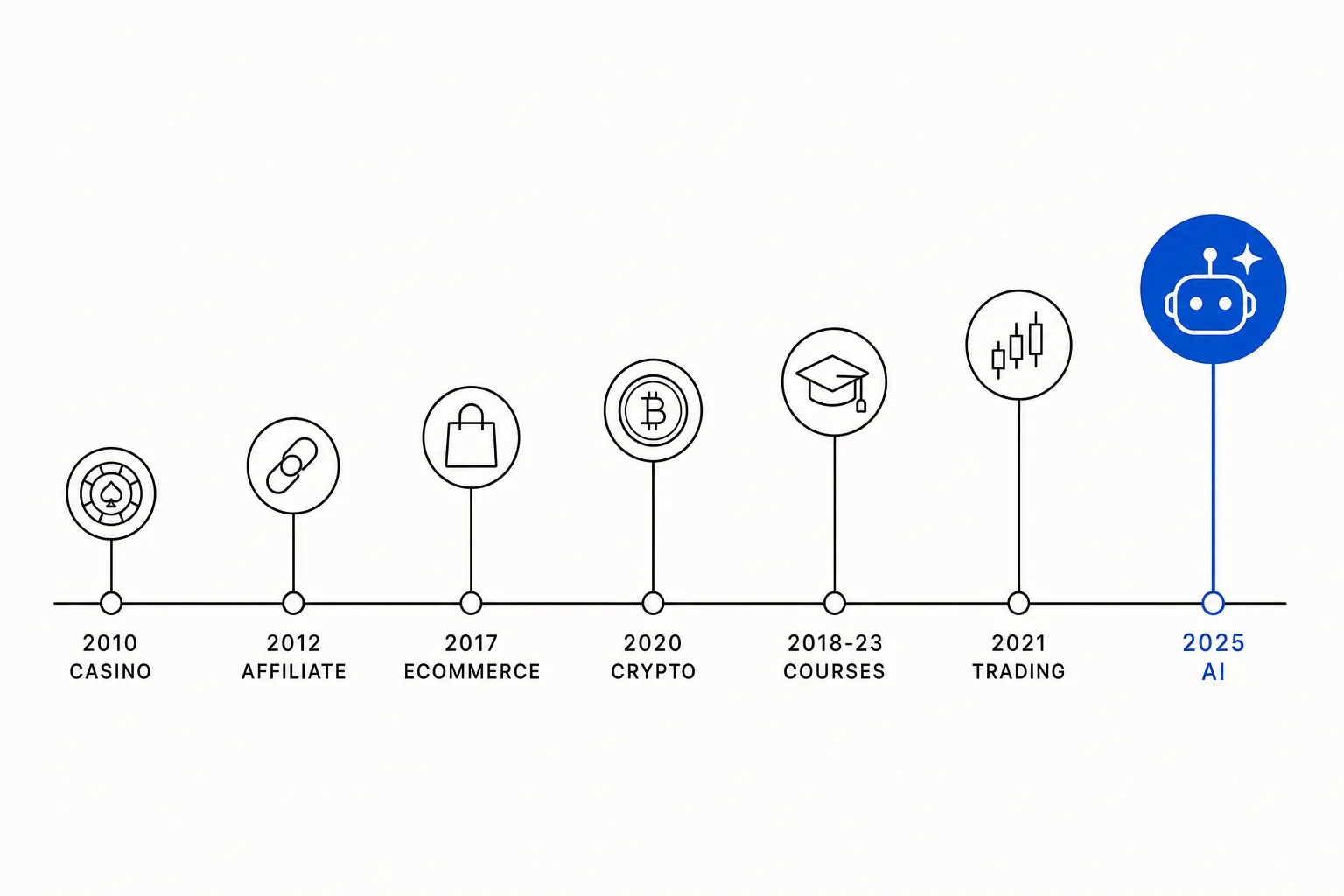

The pattern: a decade of rotating metas

Watch the mobile operator scene — the people who move to Bangkok, Dubai, Bali and chase whatever’s printing — and you see a clean rotation:

| Era | Dominant meta | What ended it |

|---|---|---|

| ~2010 | Online casino / poker + gambling affiliates | US poker ban pushed the crowd into affiliate |

| 2012–2017 | Blackhat affiliate, nutra, CPA media buying | Facebook ad tightening, tracking decay |

| 2017–2020 | Shopify dropshipping, e-commerce | iOS 14 / ATT gutted Facebook targeting |

| 2020–2022 | Crypto: DeFi, NFTs | FTX collapse |

| 2018–2023 | Influencers selling courses | Course fatigue, platform crackdowns |

| 2021–2024 | Prop-trading and “trader” funnels | Regulator action, prop-firm purge |

| 2025+ | AI | In progress |

Each wave rhymes with the last. The faces barely change.

The law underneath

An arbitrage opens, early movers extract outsized returns, the play gets commoditized and regulated, margins die, the caravan moves on.

The mobile operator is a leading indicator because they’re low-overhead, tax-flexible, and risk-tolerant — they smell the next arbitrage 12 to 18 months before it becomes a named “business model.” By the time there’s a course teaching it, the easy money is mostly gone. By the time there’s a 200,000-person community, the generic version is done.

What’s different in 2026

Every prior wave needed a human to click. The 2026 break is that AI agents now discover, decide, and pay. When AI drives the cost of making things — code, content, products — toward zero, value migrates to what stays scarce:

- Distribution — audiences, lists, un-banned ad accounts, search and answer-engine real estate

- Trust and proof — brand, track record, measurable outcomes

- Regulatory access — payments, licensing, KYC rails

- Proprietary data and workflow lock-in

A strong builder has maximum leverage to make things — but making things is now the commodity. The edge only counts when it’s bolted onto one of the scarce four.

Where AI agents actually are on the curve

Here’s where most takes go wrong. They look at the noise — the course-sellers, the “start an AI agency” funnels, the giant communities — and conclude AI automation is already saturated. That confuses operator noise with market maturity.

Go back to e-commerce in 2018. Dropshipping gurus were everywhere. It felt saturated. But e-commerce was around 14% of US retail and kept climbing past 22% over the next six years. The course noise was loud; the actual opportunity was early. Amazon FBA and Shopify minted winners for years after 2018.

AI automation is at that exact point. The demand-side numbers say early, not late:

- The AI agents market is roughly $11B in 2026, projected to ~$50B by 2030 at a ~45% CAGR — and longer forecasts run to $180B+ by 2033. Markets growing 45% a year for five-plus years are not saturated.

- Gartner: 40% of enterprise apps will embed task-specific AI agents by end of 2026, up from less than 5% in 2025. From under 1% of software being agentic in 2024 to 33% by 2028. That is the steep part of an S-curve, not the plateau.

- Only 17% of organizations have deployed AI agents so far, while 60%+ plan to within two years.

- Small business: 82–89% have invested in AI tools, but only ~8% reach advanced adoption. Almost everyone is still in the early, shallow, experimental phase.

- The verdict from the field: 2026 is the year AI moved from competitive edge to competitive baseline. Every business will need this.

That is not a saturated market. That is a market where the loud part (operators selling the dream) is running ahead of the deep part (businesses actually deploying). The gap between 8% advanced adoption and “every business will need it” is the entire opportunity, and it’s a multi-year runway.

The catch: the bar moved from “early” to “ROI”

The pushback to my own pattern is real: AI automation has years left. But the easy version is already crowded and failing, and the data is blunt about it:

- More than 40% of agentic AI projects are at risk of cancellation by 2027, on governance and cost.

- Roughly 95% of custom AI pilots fail to deliver P&L impact, and over half of CEOs report no tangible financial benefit yet.

- 68% of small businesses use AI, but most are winging it.

So both things are true at once. The market is early and enormous and the generic “I’ll build you a chatbot” offer is commoditized and mostly failing. What’s saturated isn’t the opportunity — it’s the undifferentiated operator with no vertical and no measurable outcome.

The winners in this wave are not the earliest. They’re the ones who attach to expensive, specific pain, own one vertical, and prove ROI. The move shifts from show up first to deliver a number the client can see.

What to actually do

- Don’t read the noise as the market. Course volume is a lagging indicator of hype, not a measure of demand. The demand curve on AI automation is still climbing hard.

- Go vertical and prove ROI. With 95% of generic pilots failing, the entire edge is measurable outcomes in one industry you understand. That’s where the next five years of money is.

- Be the pickaxe where you can. Every operator entering this wave needs infrastructure, templates, and tooling. Selling to the operator army is a more durable position than competing in it.

- Own a distribution channel. In a world where everyone can build an agent, the one who owns the audience wins. That’s the through-line of every wave on this list.

The meta rotated to AI, and unlike the courses-and-crypto waves, this one has a real, multi-year demand curve underneath it. It just stopped rewarding the people who only know how to be early.